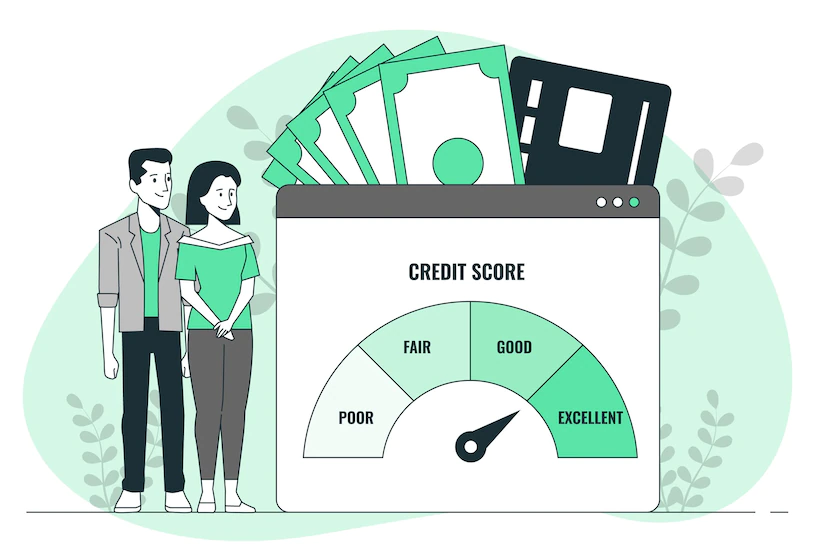

Credit Score: Things to Know Before Taking Out a Loan

A healthy credit score is the key to financial peace of mind. So, whether you are looking to purchase a new house or a vehicle, start a business or start planning for retirement, nothing is more important than maintaining a healthy credit score. As your first step towards achieving a healthy credit score, it’s important to know what’s in your credit report.

In this blog post, we will take a look at everything you need to know about your credit score. Let’s get started!

How to check your credit score?

It’s important to know your credit score because it is a number that lenders use to determine your creditworthiness. A high credit score means you’re a low-risk borrower, which could lead to a lower interest rate on a loan.

A low credit score could lead to a higher interest rate and could mean you won’t be approved for a loan at all. You can check your credit score for free with a credit report from one of the three major credit bureaus: Equifax, Experian and TransUnion. You can also use a credit monitoring service, such as Credit Karma or Credit Sesame, which will give you your credit score from TransUnion and Equifax.

What factors affect your credit score?

Credit scores are important because they represent your creditworthiness to lenders. A high credit score means you’re a low-risk borrower, which could translate to lower interest rates on loans and credit cards. A low credit score could make it more difficult for you to qualify for a loan or get a credit card with a favorable interest rate. There are many different factors that affect your credit score. Some of the most important include: –

- Your payment history. This is the biggest factor in your credit score. Lenders want to see that you’re a responsible borrower who pays your bills on time.

- Your credit utilization. This is the amount of credit you’re using compared to the amount of credit you have available. It’s a good idea to keep your credit utilization low, so lenders see that you’re not maxing out your credit cards.

- Your credit mix. This refers to the different types of credit you have, such as revolving credit (like credit cards) and installment loans (like car loans). A mix of different types of credit can help your score. -Your length of credit history. This is a measure of how long you’ve been using credit. A longer credit history is generally better for your score.

- Your new credit applications. Whenever you apply for a new credit card or loan, lenders do a hard inquiry on your credit report. This can temporarily lower your score.

- Your length of credit history. This is a measure of how long you’ve been using credit. A longer credit history is generally better for your score.

How your credit score affects your loan eligibility?

A credit score is a number that represents the creditworthiness of an individual. It is used by lenders to determine whether an individual is eligible for a loan. The higher the credit score, the more likely an individual is to be approved for a loan.

A lower credit score may result in an individual being denied for a loan. There are a number of factors that can impact an individual’s credit score, including payment history, credit utilization, and length of credit history.

How to improve your credit score?

There are a few things you can do to improve your credit score. One is to make sure you keep updated on your credit score rating and credit utilization levels. You can do this by monitoring your credit report and credit score rating on a regular basis.

You can also keep your credit utilization levels low by using credit wisely and paying off your balances in full each month. Another way to improve your credit score is to have a good mix of different types of credit, such as revolving credit and instalment credit. You can also try to get a secured credit card to help build your credit history. Check out here a detailed guide on 3 Ways to Boost Your Credit Score.

Why your credit score matters?

Your credit score is one of the most important pieces of financial information about you. It is a number that represents your creditworthiness and is used by lenders to determine whether to give you credit and what interest rate to charge you.

A good credit score can save you thousands of dollars in interest over the life of a loan. A bad credit score can cost you a loan altogether. Your credit score is important because it is one of the factors that lenders look at when considering you for a loan. The higher your credit score, the lower the interest rate you will be offered. This can save you thousands of dollars over the life of a loan.

A low credit score may mean you are not offered a loan at all. Your credit score is also important because it can affect your ability to rent an apartment, get insurance, or even get a job. Landlords, insurers, and employers often look at credit scores when making decisions about whether to offer someone a lease, insurance policy, or job.

A good credit score can give you an edge over other candidates. You can get your credit score from any of the three major credit reporting agencies: Equifax, Experian, and TransUnion. You can also get your credit score from some banks and credit card companies.

How to use your credit score to get the best loan terms?

Credit scores are important when it comes to getting the best loan terms. A high credit score means you’re a low-risk borrower, which could lead to a lower interest rate on your loan. A lower interest rate could save you thousands of dollars over the life of your loan.

There are a few things you can do to help improve your credit score.

- First, make sure you keep up with your payments. Paying your bills on time is one of the most important factors in determining your credit score. You should also try to keep your balances low.

- High balances can hurt your credit score. If you’re looking to take out a loan, shop around.

- Compare rates from different lenders to see who can offer you the best terms. And be sure to check your credit score before you apply. Knowing your score can help you get the best loan terms possible.

At Nutshell

If you’re thinking about taking out a loan, you should know your credit score. Your credit score is a three-digit number that helps lenders and insurance companies evaluate the risk of lending you money. A good credit score can help you qualify for a loan with a lower interest rate, while a bad credit score may make you ineligible for a low-interest loan. But how can you get your credit score? In this post, I’m going to walk you through the whole process. Keep reading and I’ll keep you posted on how my credit score is doing!

![Tamil Aunty WhatsApp Group Link List [100% Active]](https://writofly.com/wp-content/uploads/https://images.pexels.com/photos/10070972/pexels-photo-10070972.jpeg?auto=compress&cs=tinysrgb&dpr=2&h=650&w=940)